Introduction

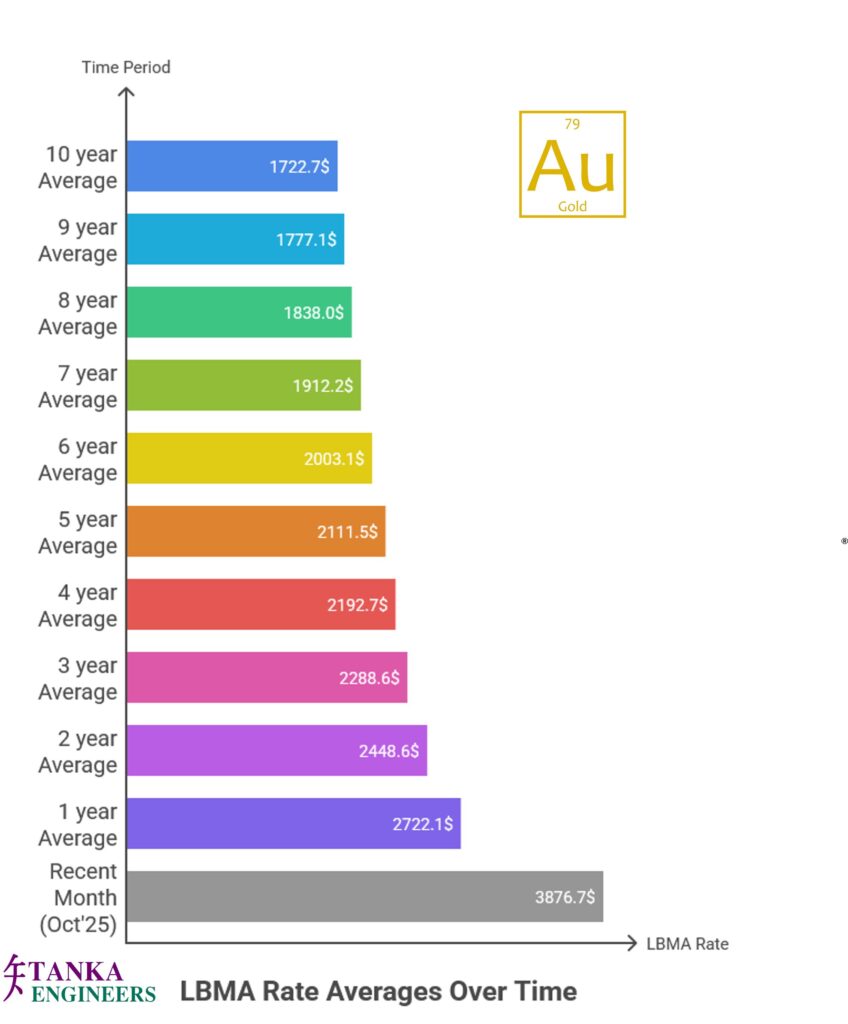

Gold price assumptions are a critical foundation in every mining financial model. The selected price influences project valuation, investment decisions, and financing outcomes, regardless of whether the project is at the early-stage study phase, approaching development, undergoing expansion, or under evaluation for acquisition. The recent rise in gold prices to approximately $3,800 per ounce, compared to the 10-year average of $1,700 per ounce, demonstrates the commodity’s volatility and the inherent difficulty in selecting a realistic and defensible price for long-term financial projections.

Current Market Context

Since early 2023, the gold market has seen a sustained, month-by-month increase. Prices have climbed from $61 per gram in January 2023 to $124 per gram in October 2025, effectively doubling within less than three years. Monthly fluctuations of up to 8–10% highlight the sensitivity of mining project economics to changes in gold price. This upward trend is evident in several recent high-profile transactions:

- Gold Fields – Gold Road: approximately US$2.4 billion

- Red 5 – Silver Lake merger: approximately US$2.2 billion

- Porcupine Mine sale: approximately US$425 million

- Coffee Project sale: up to US$150 million

- Zijin Gold IPO (2025): valuation exceeding US$40 billion

These deals have been completed in a high-price environment, but historical cycles suggest that commodity prices eventually correct. Projects that appear profitable at peak prices may face challenges when prices move back towards long-term averages.

Guiding Principles for Gold Price Selection

Early-Stage Projects

For early-stage projects, it is prudent to use long-term average gold prices (5–10 years) as the basis for financial modelling. This approach ensures conservative valuations before significant exploration or study capital is committed.

Near-to-Development Projects (DFS/FS)

A balanced strategy is recommended for near-to-development projects by utilising 2–3 year averages as the base case, while applying long-term averages in downside scenarios. This methodology meets investor and lender expectations, providing credibility and robust, stress-tested economics.

Expansion Projects

For expansion projects, shorter-term averages (1–3 years) may be considered, reflecting shorter payback periods and reduced capital risk due to existing infrastructure. However, it remains essential to stress-test with long-term averages to confirm the resilience of project economics.

Acquisitions

Valuations for acquisitions should be grounded on long-term consensus pricing (5-year averages) to prevent overpayment during periods of elevated prices. While sellers may prefer shorter-term benchmarks, disciplined buyers must ensure their valuations are defensible under conservative assumptions.

Fundamental Principle

The core principle is clear: Net Present Values (NPVs) and Internal Rates of Return (IRRs) must remain defensible throughout market cycles, not just during price peaks. Employing a layered approach—using long-term averages for base cases, shorter-term averages for upside scenarios, and applying stress-testing for downside cases—establishes a robust framework for feasibility studies and acquisition assessments.

Conclusion

In the current environment of elevated gold prices, rigorous financial modelling is indispensable. At Tanka Engineers LLP, we employ price averaging, month-by-month sensitivity analysis, and multi-scenario modelling in every feasibility study and acquisition review. This ensures that our clients’ projects are evaluated with realism and resilience, and are aligned with global best practices under the JORC and NI 43-101 standards.